444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

Market Overview

The Asia Pacific Oil and Gas CAPEX Market refers to the market for capital expenditures in the oil and gas industry across the Asia Pacific region. Capital expenditures, or CAPEX, are investments made by oil and gas companies in new projects, equipment, and infrastructure to support their operations and growth. The Asia Pacific region is known for its significant oil and gas reserves and is a crucial player in the global energy landscape.

Meaning

CAPEX stands for capital expenditures, which are investments made by companies in long-term assets such as property, plant, and equipment. In the context of the oil and gas industry, CAPEX refers to the funds allocated by companies to develop new oil and gas fields, construct pipelines and refineries, and upgrade existing infrastructure. These investments are essential for expanding production capacity, exploring new reserves, and maintaining operational efficiency.

Executive Summary

The Asia Pacific Oil and Gas CAPEX Market is witnessing significant growth due to several factors. This market analysis provides key insights into the market drivers, restraints, and opportunities, along with an evaluation of market dynamics, regional analysis, competitive landscape, segmentation, and category-wise insights. It also includes a SWOT analysis, key trends, the impact of Covid-19, industry developments, analyst suggestions, future outlook, and a conclusion.

Important Note: The companies listed in the image above are for reference only. The final study will cover 18–20 key players in this market, and the list can be adjusted based on our client’s requirements.

Key Market Insights

Upstream Dominance: Over 45% of total CAPEX is allocated to exploration and production, with deepwater developments in the South China Sea and shale gas projects in China and Australia leading the spend.

LNG Surge: Asia Pacific accounts for more than 70% of global LNG import capacity; investments in new liquefaction trains (e.g., Papua LNG, Ichthys) and regasification terminals in India, Pakistan, and Vietnam are driving midstream CAPEX.

Refinery Modernization: Aging refining complexes in India and China are undergoing upgrades to produce cleaner fuels and petrochemicals, supported by PPP models and green-financing mechanisms.

Digital Transformation: Operators are allocating up to 10% of their CAPEX budgets to advanced analytics, IoT sensors, and automation to reduce operating costs by 15–20% and extend asset life.

Carbon Management: A rising share of CAPEX is earmarked for carbon capture, utilization, and storage (CCUS) and blue hydrogen pilots, reflecting national decarbonization roadmaps.

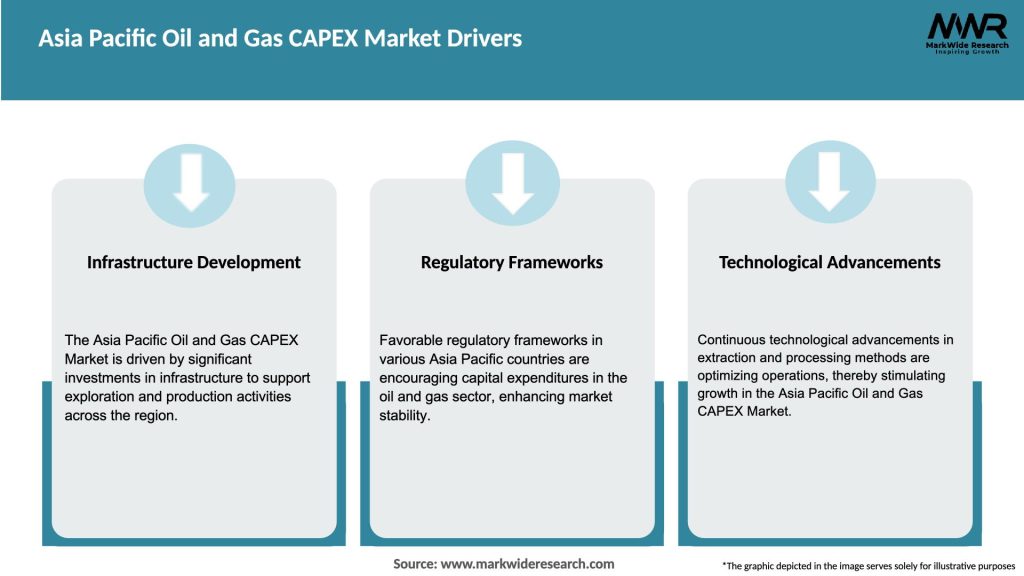

Market Drivers

Energy Demand Growth: Rapid industrialization, urbanization, and rising standards of living are pushing regional oil and gas consumption upward, prompting capacity expansions.

Strategic Energy Security: Governments in China, India, Japan, and South Korea are investing in domestic E&P and diversified import infrastructure to mitigate geopolitical risks.

LNG Trade Dynamics: Asia’s position as the world’s largest LNG importer incentivizes construction of liquefaction and regasification facilities to capture spot and long-term market opportunities.

Downstream Integration: The push for petrochemical self-sufficiency is driving integrated refining-petrochemical complexes, which offer higher margins and value addition.

Technology Adoption: CAPEX on digital oilfield technologies, robotics, and automation is rising to offset labor constraints and improve operational efficiency across remote and offshore assets.

Market Restraints

Volatile Oil Prices: Fluctuating crude benchmarks can delay or downsize CAPEX commitments, particularly for high-cost deepwater or Arctic projects.

Regulatory Hurdles: Stringent environmental approvals, local content requirements, and licensing delays can extend project timelines and inflate costs.

Financing Challenges: Access to affordable capital is constrained by lenders’ growing ESG concerns, leading to higher funding costs for carbon-intensive projects.

Supply Chain Disruptions: Global shortages of specialized equipment and logistical bottlenecks—exacerbated by the pandemic—can push back project start-ups by months or years.

Community Opposition: Social license considerations, including indigenous rights and environmental activism, can introduce project cancellations or scope reductions.

Market Opportunities

Greenfield Investments: Undeveloped basins in Myanmar, Myanmar, and East Timor offer first-mover advantages for explorers and service contractors.

Repurposing Assets: Decommissioned offshore platforms can be converted to carbon storage sites or wind-turbine foundations, creating circular CAPEX opportunities.

Hydrogen Hubs: Joint ventures between oil majors and governments to develop blue and green hydrogen infrastructure can leverage existing midstream networks.

Small-Scale LNG: Mini-LNG plants and floating storage regasification units (FSRUs) present lower-CAPEX entry points for emerging importers.

Digital Retrofits: Legacy facilities can be upgraded with advanced control systems and predictive-maintenance platforms to defer heavy CAPEX.

Market Dynamics

Public-Private Partnerships (PPPs): Collaborative CAPEX financing models are becoming prevalent for large downstream and midstream projects to share risk and leverage private efficiency.

Localization Mandates: National content requirements in Australia, Malaysia, and Indonesia drive CAPEX towards local fabrication, engineering, and service industries.

Decarbonization Policies: ASEAN and APEC decarbonization targets channel CAPEX into low-carbon pilot projects and CCUS demonstration plants.

M&A Activity: Consolidation among E&P firms and joint ventures between state-owned enterprises bolster integrated CAPEX strategies and portfolio optimization.

Risk Management: Hedge and offtake agreements are being used to secure revenue streams and underwrite CAPEX, especially in LNG and petrochemicals.

Regional Analysis

Within Asia Pacific:

Southeast Asia: CAPEX focuses on offshore gas developments (Malaysia, Indonesia) and FSRU deployments in the Philippines and Vietnam.

Northeast Asia: Japan and South Korea invest primarily in downstream refineries, petrochemical plants, and upstream overseas joint ventures.

South Asia: India’s CAPEX is split between refinery modernization, pipeline expansions (Jagadishpur–Haldia), and newly sanctioned shale-gas pilot schemes.

Australasia: Australia leads in LNG CAPEX, with major trains at Wheatstone, LNG Northern, and forthcoming Scarborough developments.

China: Balanced CAPEX across shale E&P in Sichuan, deepwater offshore fields, midstream trunk pipelines (e.g., West–East Gas Pipeline), and high-conversion petrochemicals.

Competitive Landscape

Leading Companies in the Asia Pacific Oil and Gas CAPEX Market:

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

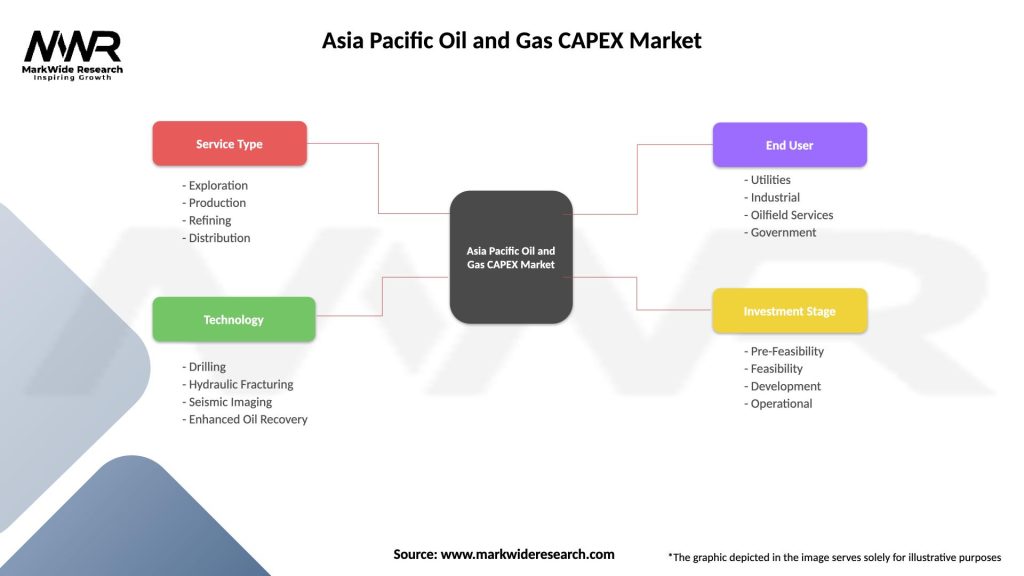

Segmentation

The Asia Pacific Oil and Gas CAPEX Market can be segmented based on the type of investment, including upstream exploration and production, midstream infrastructure, and downstream refining and petrochemicals. The market can also be segmented by country, with key markets being China, India, Australia, Indonesia, Malaysia, and Thailand. Additionally, the market can be categorized based on the type of energy source, such as oil, natural gas, and LNG.

Category-wise Insights

In the upstream segment, investments are primarily directed towards exploring and developing new oil and gas fields. In the midstream segment, investments focus on constructing pipelines, LNG terminals, and storage facilities to transport and store oil and gas. In the downstream segment, investments are made in refineries, petrochemical plants, and distribution networks to process and distribute refined products to end consumers. Each category offers unique growth opportunities and challenges.

Key Benefits for Industry Participants and Stakeholders

Industry participants and stakeholders in the Asia Pacific Oil and Gas CAPEX Market can benefit from the market’s growth potential. Investments in the market can generate substantial returns and contribute to energy security and economic development. Companies involved in exploration and production can gain from the development of new reserves, while infrastructure providers can benefit from the expansion of pipelines and terminals. Governments and local communities can also gain from job creation and revenue generation.

SWOT Analysis

Strengths:

Weaknesses:

Opportunities:

Threats:

Market Key Trends

Several key trends are shaping the Asia Pacific Oil and Gas CAPEX Market. These include the increasing use of digital technologies and automation in oil and gas operations, the focus on cost optimization and operational efficiency, the integration of renewable energy and low-carbon technologies, and the emergence of new business models and partnerships. Market players are also investing in research and development to enhance exploration techniques, reduce environmental impact, and improve overall performance.

Covid-19 Impact

The Covid-19 pandemic has had a significant impact on the oil and gas industry worldwide, including the Asia Pacific region. The lockdown measures and travel restrictions imposed to curb the spread of the virus resulted in a sharp decline in oil and gas demand, leading to a collapse in prices. Many projects were delayed or put on hold, and companies faced financial challenges. However, as economies recover and energy demand rebounds, the market is expected to regain momentum, supported by government stimulus measures and infrastructure investments.

Key Industry Developments

Papua LNG FID (2023): Major CAPEX sanction of a 9 mtpa floating LNG project in Indonesia, totaling over USD 12 billion.

India’s National Gas Grid: USD 5 billion midstream CAPEX plan to expand gas pipelines by over 10,000 km through 2030.

Australia’s Hydrogen Hubs: AUD 20 billion in government and private CAPEX commitments for green hydrogen corridors linking renewables to export terminals.

Analyst Suggestions

Adopt Modular Strategies: Favor modularized facilities and floating assets to de-risk large CAPEX outlays and accelerate commissioning.

Align with Transition Goals: Co-invest in CCUS and hydrogen alongside traditional CAPEX to access green financing and public incentives.

Leverage Digital Planning: Use digital-twin and advanced analytics during front-end engineering design (FEED) to optimize CAPEX schedules and budgets.

Strengthen Local Partnerships: Engage early with local contractors and equipment suppliers to satisfy content requirements and reduce lead times.

Future Outlook

The Asia Pacific Oil and Gas CAPEX Market is expected to witness steady growth in the coming years. The region’s growing energy demand, abundant reserves, and supportive government policies will continue to drive investments. However, market players must navigate challenges related to environmental concerns, geopolitical risks, and the energy transition. The adoption of new technologies, the development of unconventional resources, and the expansion of natural gas infrastructure will shape the future landscape of the market.

Conclusion

In conclusion, the Asia Pacific Oil and Gas CAPEX Market presents significant opportunities for industry participants and stakeholders. The market’s growth is driven by increasing energy demand, investments in exploration and production, and favorable government policies. However, challenges such as environmental concerns and geopolitical uncertainties must be addressed. By embracing advanced technologies, diversifying portfolios, and prioritizing sustainability, companies can thrive in this dynamic market. The future outlook remains positive, with continued investments expected to meet the region’s energy needs and drive economic development.

What is Oil and Gas CAPEX?

Oil and Gas CAPEX refers to the capital expenditures made by companies in the oil and gas sector for the development and maintenance of their assets. This includes investments in exploration, drilling, production facilities, and infrastructure.

What are the key players in the Asia Pacific Oil and Gas CAPEX Market?

Key players in the Asia Pacific Oil and Gas CAPEX Market include companies like Woodside Petroleum, Santos, and Oil Search, which are involved in various stages of oil and gas exploration and production, among others.

What are the main drivers of the Asia Pacific Oil and Gas CAPEX Market?

The main drivers of the Asia Pacific Oil and Gas CAPEX Market include increasing energy demand, technological advancements in extraction methods, and the need for infrastructure development to support growing production capacities.

What challenges does the Asia Pacific Oil and Gas CAPEX Market face?

Challenges in the Asia Pacific Oil and Gas CAPEX Market include fluctuating oil prices, regulatory hurdles, and environmental concerns that can impact investment decisions and project viability.

What opportunities exist in the Asia Pacific Oil and Gas CAPEX Market?

Opportunities in the Asia Pacific Oil and Gas CAPEX Market include the potential for renewable energy integration, advancements in carbon capture technologies, and the exploration of untapped reserves in offshore regions.

What trends are shaping the Asia Pacific Oil and Gas CAPEX Market?

Trends shaping the Asia Pacific Oil and Gas CAPEX Market include a shift towards digitalization in operations, increased focus on sustainability practices, and the adoption of innovative drilling technologies to enhance efficiency.

Asia Pacific Oil and Gas CAPEX Market

| Segmentation Details | Description |

|---|---|

| Service Type | Exploration, Production, Refining, Distribution |

| Technology | Drilling, Hydraulic Fracturing, Seismic Imaging, Enhanced Oil Recovery |

| End User | Utilities, Industrial, Oilfield Services, Government |

| Investment Stage | Pre-Feasibility, Feasibility, Development, Operational |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading Companies in the Asia Pacific Oil and Gas CAPEX Market:

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.