444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

Market Overview

The Algeria oil and gas downstream market plays a crucial role in the country’s economy. With significant reserves of oil and natural gas, Algeria has established itself as a key player in the global energy market. The downstream sector encompasses activities such as refining, distribution, marketing, and retailing of petroleum products. This sector is vital for meeting the domestic energy demands and driving economic growth through exports.

Meaning

The term “downstream” refers to the processes involved in converting crude oil and natural gas into various refined products that are ready for consumption. It encompasses refining operations, where crude oil is processed to extract valuable products like gasoline, diesel, jet fuel, and petrochemicals. The downstream sector also includes storage, transportation, and distribution of these refined products to end-users, such as industries, households, and the transportation sector.

Executive Summary

The Algeria oil and gas downstream market has experienced significant growth in recent years. The country’s rich reserves of hydrocarbons, coupled with increasing domestic and international demand, have propelled the growth of the downstream sector. The government has implemented several reforms to attract foreign investment, improve infrastructure, and enhance the efficiency of the downstream value chain.

Important Note: The companies listed in the image above are for reference only. The final study will cover 18–20 key players in this market, and the list can be adjusted based on our client’s requirements.

Key Market Insights

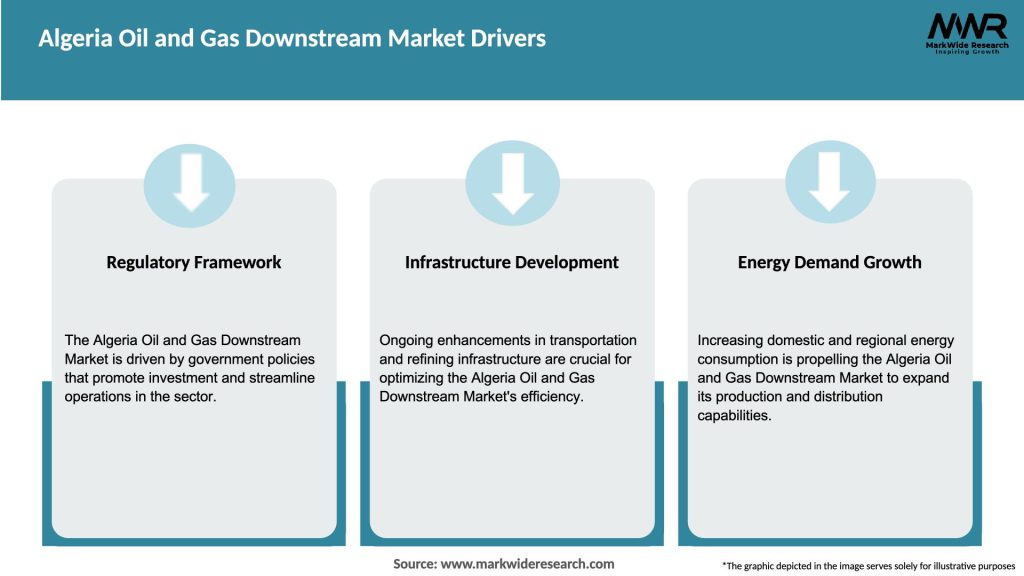

Market Drivers

Several factors are driving the growth of the Algeria oil and gas downstream market:

Market Restraints

Despite the positive growth prospects, the Algeria oil and gas downstream market faces some challenges:

Market Opportunities

The Algeria oil and gas downstream market offers several opportunities for industry players:

Market Dynamics

The Algeria oil and gas downstream market is characterized by dynamic factors that influence its growth:

Regional Analysis

The Algeria oil and gas downstream market is mainly concentrated in key regions:

Competitive Landscape

Leading Companies in the Algeria Oil and Gas Downstream Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

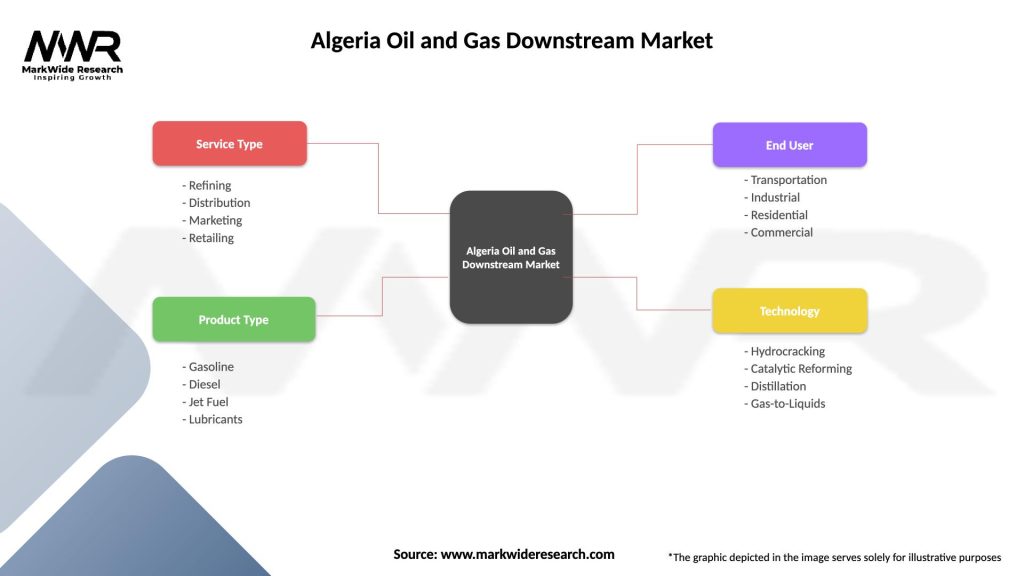

Segmentation

The Algeria oil and gas downstream market can be segmented based on various criteria:

Category-wise Insights

Key Benefits for Industry Participants and Stakeholders

SWOT Analysis

Market Key Trends

Covid-19 Impact

The Covid-19 pandemic had a significant impact on the Algeria oil and gas downstream market. The restrictions imposed to contain the virus, such as lockdowns and reduced economic activity, resulted in a decline in energy demand and disrupted supply chains. The market experienced a temporary slowdown, affecting refining operations, distribution, and export activities. However, as economic activities resume and global energy demand recovers, the market is expected to regain momentum.

Key Industry Developments

Analyst Suggestions

Future Outlook

The future outlook for the Algeria oil and gas downstream market is positive. The country’s rich reserves, government initiatives, and strategic location provide a solid foundation for growth. With efforts to modernize infrastructure, attract foreign investment, and diversify downstream activities, the market is poised for expansion. However, challenges such as aging infrastructure and regulatory complexities need to be addressed to fully realize the market’s potential.

Conclusion

The Algeria oil and gas downstream market plays a crucial role in meeting the country’s energy demands and driving economic growth. With abundant reserves of oil and natural gas, Algeria has the potential to become a major player in the global energy market. The market offers opportunities for profitability, collaboration, and diversification, while also facing challenges such as aging infrastructure and regulatory complexities. By embracing technology, sustainable practices, and strategic partnerships, industry participants can navigate the market dynamics and contribute to the growth and development of the Algeria oil and gas downstream sector.

What is Oil and Gas Downstream?

Oil and Gas Downstream refers to the processes involved in refining crude oil and processing natural gas, as well as the distribution and sale of petroleum products. This includes activities such as refining, marketing, and retailing of fuels and lubricants.

What are the key players in the Algeria Oil and Gas Downstream Market?

Key players in the Algeria Oil and Gas Downstream Market include Sonatrach, the national oil company, and international firms like TotalEnergies and Eni. These companies are involved in refining, distribution, and retailing of oil and gas products, among others.

What are the growth factors driving the Algeria Oil and Gas Downstream Market?

The growth of the Algeria Oil and Gas Downstream Market is driven by increasing domestic energy demand, investments in refining capacity, and the expansion of distribution networks. Additionally, government initiatives to enhance energy security play a significant role.

What challenges does the Algeria Oil and Gas Downstream Market face?

The Algeria Oil and Gas Downstream Market faces challenges such as aging infrastructure, regulatory hurdles, and competition from alternative energy sources. These factors can hinder operational efficiency and investment attractiveness.

What opportunities exist in the Algeria Oil and Gas Downstream Market?

Opportunities in the Algeria Oil and Gas Downstream Market include the potential for modernization of refineries, the introduction of cleaner technologies, and the expansion of export markets. These factors can enhance profitability and sustainability.

What trends are shaping the Algeria Oil and Gas Downstream Market?

Trends in the Algeria Oil and Gas Downstream Market include a shift towards digitalization, increased focus on sustainability, and the adoption of advanced refining technologies. These trends aim to improve efficiency and reduce environmental impact.

Algeria Oil and Gas Downstream Market

| Segmentation Details | Description |

|---|---|

| Service Type | Refining, Distribution, Marketing, Retailing |

| Product Type | Gasoline, Diesel, Jet Fuel, Lubricants |

| End User | Transportation, Industrial, Residential, Commercial |

| Technology | Hydrocracking, Catalytic Reforming, Distillation, Gas-to-Liquids |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading Companies in the Algeria Oil and Gas Downstream Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.