444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

Market Overview:

The UK home insurance market is a dynamic and competitive industry that provides financial protection to homeowners against potential risks and damages to their properties. Home insurance policies cover a range of perils, including fire, theft, natural disasters, and liability claims. With a significant number of households in the UK, the demand for home insurance remains robust.

Meaning:

Home insurance, also known as homeowners insurance, is a type of property insurance that offers coverage for damages or losses to a residential property and its contents. It provides financial compensation to homeowners in the event of unforeseen incidents, such as theft, fire, vandalism, or natural disasters. Home insurance policies can vary in coverage and price, depending on factors like the property’s location, size, construction type, and the level of protection desired by the homeowner.

Executive Summary:

The UK home insurance market continues to experience steady growth, driven by the increasing awareness among homeowners about the importance of protecting their properties. The market is highly competitive, with several insurance providers offering a wide range of coverage options and customized policies to cater to the diverse needs of homeowners. Rising property values and an increase in the number of households are driving the demand for home insurance in the country. However, the market also faces challenges such as rising claims costs and regulatory changes that impact insurers’ profitability.

Important Note: The companies listed in the image above are for reference only. The final study will cover 18–20 key players in this market, and the list can be adjusted based on our client’s requirements.

Key Market Insights:

Market Drivers:

Market Restraints:

Market Opportunities:

Market Dynamics:

The UK home insurance market is driven by a combination of factors, including changing consumer preferences, economic conditions, regulatory changes, and advancements in technology. The market is highly competitive, with insurance providers continuously innovating to meet the evolving needs of homeowners. Understanding and adapting to market dynamics is crucial for insurance companies to maintain a strong market position and capitalize on emerging opportunities.

Regional Analysis:

The UK home insurance market exhibits regional variations based on factors such as population density, property values, and local risk profiles. Urban areas with higher population concentrations and higher property values tend to have higher demand for home insurance. Additionally, regions prone to specific risks, such as flooding or subsidence, may experience variations in insurance pricing and coverage availability. Insurance companies consider regional factors when underwriting policies and determining premiums.

Competitive Landscape:

Leading Companies in the UK Home Insurance Market:

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

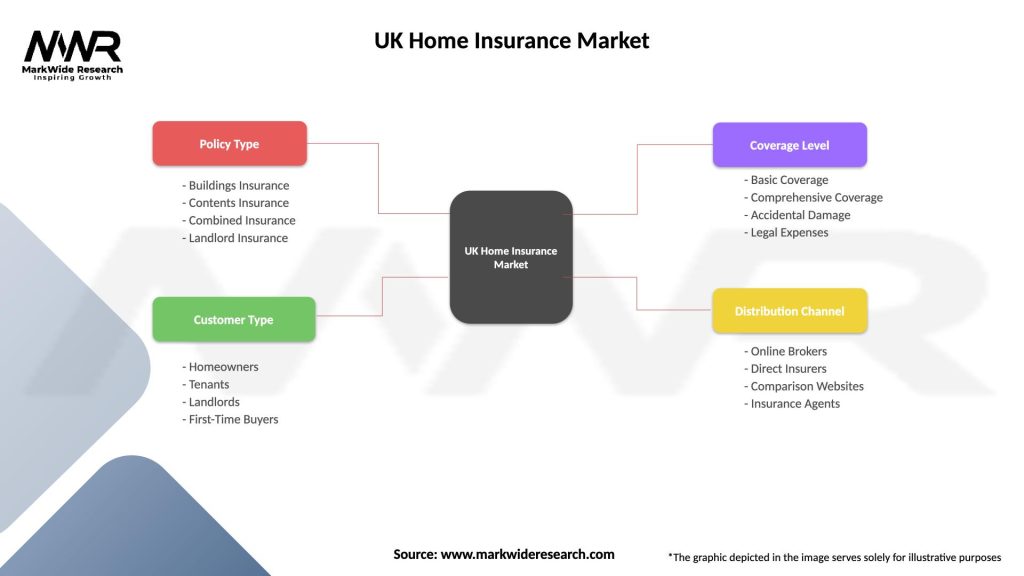

Segmentation:

The UK home insurance market can be segmented based on various criteria, including policy type, coverage options, property type, and customer demographics. Segmentation allows insurance providers to tailor their offerings to different customer segments and offer customized coverage options that meet specific needs.

Category-wise Insights:

Key Benefits for Industry Participants and Stakeholders:

SWOT Analysis:

Market Key Trends:

Covid-19 Impact:

The Covid-19 pandemic has had a significant impact on the UK home insurance market. The increase in remote working and spending more time at home has led to heightened awareness of home-related risks, driving the demand for insurance coverage. However, insurers have also faced challenges in assessing risks associated with remote working, property maintenance, and changes in property usage patterns. The pandemic has highlighted the importance of adapting policies to accommodate evolving risks and customer needs.

Key Industry Developments:

Analyst Suggestions:

Future Outlook:

The future of the UK home insurance market appears promising, with steady growth expected. Technological advancements, customized policy offerings, and a focus on customer-centric experiences will shape the market’s trajectory. Insurance companies that adapt to emerging trends, effectively manage risks, and provide innovative solutions will be well-positioned to thrive in this competitive industry.

Conclusion:

The UK home insurance market offers essential financial protection for homeowners, providing coverage against potential risks and damages to their properties and belongings. The market is characterized by strong demand, intense competition, and continuous innovation. Insurance companies must navigate regulatory changes, rising claims costs, and emerging risks while leveraging technological advancements to enhance operational efficiency and customer experiences. By adapting to market dynamics, focusing on customer needs, and embracing digital transformation, insurers can capitalize on the opportunities in the UK home insurance market and secure long-term success in an evolving industry.

What is Home Insurance?

Home insurance is a type of property insurance that covers private residences. It provides financial protection against damages to the home and its contents, as well as liability coverage for accidents that occur on the property.

What are the key players in the UK Home Insurance Market?

Key players in the UK Home Insurance Market include companies like Aviva, Direct Line, and Legal & General. These companies offer a range of policies tailored to different customer needs, among others.

What are the main drivers of the UK Home Insurance Market?

The main drivers of the UK Home Insurance Market include the increasing awareness of property protection, rising property values, and the growing incidence of natural disasters. Additionally, the demand for customized insurance solutions is also contributing to market growth.

What challenges does the UK Home Insurance Market face?

The UK Home Insurance Market faces challenges such as rising claims costs due to climate change and increased competition among insurers. Additionally, regulatory changes and consumer expectations for more flexible policies can also pose challenges.

What opportunities exist in the UK Home Insurance Market?

Opportunities in the UK Home Insurance Market include the potential for digital transformation and the integration of smart home technology. Insurers can leverage data analytics to offer personalized policies and improve customer engagement.

What trends are shaping the UK Home Insurance Market?

Trends shaping the UK Home Insurance Market include the rise of usage-based insurance models and the increasing importance of sustainability in policy offerings. Additionally, the adoption of artificial intelligence for claims processing is becoming more prevalent.

UK Home Insurance Market

| Segmentation Details | Description |

|---|---|

| Policy Type | Buildings Insurance, Contents Insurance, Combined Insurance, Landlord Insurance |

| Customer Type | Homeowners, Tenants, Landlords, First-Time Buyers |

| Coverage Level | Basic Coverage, Comprehensive Coverage, Accidental Damage, Legal Expenses |

| Distribution Channel | Online Brokers, Direct Insurers, Comparison Websites, Insurance Agents |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading Companies in the UK Home Insurance Market:

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.